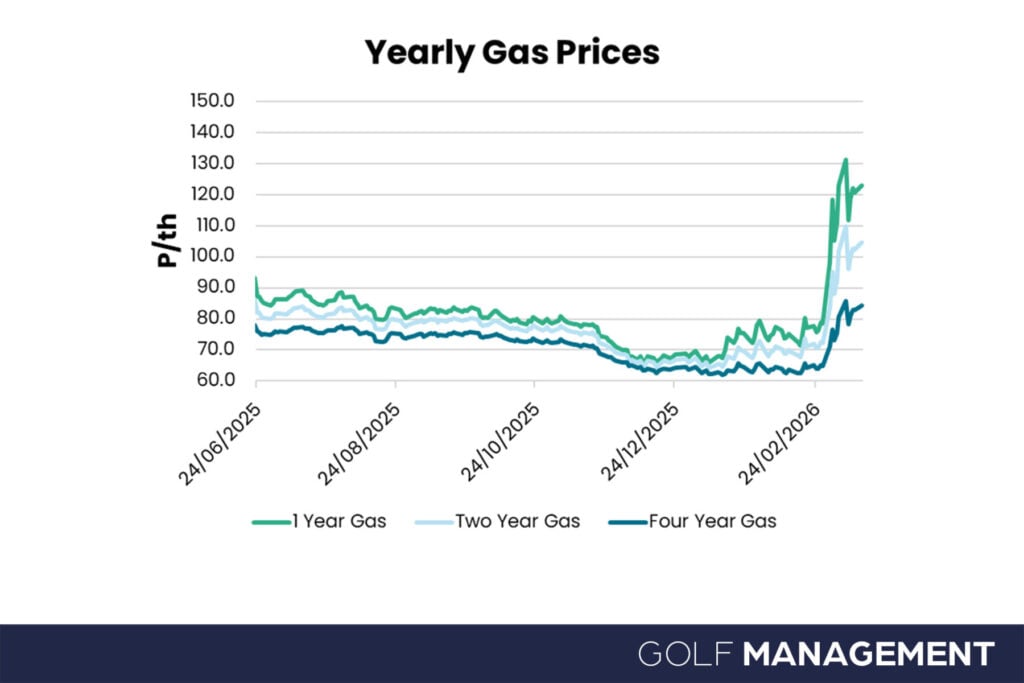

The conflict in the Middle East has added a significant premium to the front of the gas and power curves.

However, prices further out on the curve still look attractive, with many longer-dated contracts still below the 12-month averages – but they have been creeping higher in recent days.

Europe has come out of this winter with storage already severely depleted. Overall stocks are less than 30 per cent full – the lowest storage since 2022. The markets we’re closest to are even more bleak with the Netherlands at 9 per cent and Germany at 20 per cent.

The most significant impact from the Middle East comes from Qatar, the world’s second largest LNG supplier. Its Ras Laffan gas facility was hit on March 2, 2026 and Qatar Energy immediately called a force majeure on their gas supply contracts. They have subsequently stated that the facility will not restart while the conflict is ongoing. Once restarted, this would then take weeks to months to start producing LNG again.

Qatar supplies over 20per cent of the world’s LNG and while only 20 per cent of this comes to Europe, the rest goes largely to the mature LNG markets of the Far East. These markets have a considerable LNG dependency, which peaks in mid-summer and mid-winter as cooling and heating drive demand.

With just the loss of Qatari LNG, Europe’s storage filling dynamics are looking incredibly tight with projections pointing to just 58 per cent full by the end of the summer.

This is just the loss of Qatari gas into Europe and doesn’t account for the significant spot demand that will come from Asia to make up for their lost cargoes.

Competition for LNG this summer will pick up as temperatures increase in the Far East. This was the trigger that caused prices to rise in the summer of 2022, as LNG headed to higher-priced markets. The risk is that it happens again. This caused longer dated power positions to rise to 4-6x the levels that they are today.

With Qatar confirming that they will not restart deliveries until the conflict is over, looking at the duration of recent Middle Eastern conflicts in Syria, Lebanon, Gaza, Iraq and Afghanistan – as well as the steep backwardation in the curve (discounts on future prices) – my advice is to go to market and go for as long as you can.

The carbon price has corrected to the lowest levels in the last 12 months. This has meant that gas prices have risen more than power prices and add to the value in longer-term power prices.

The front of the curve has seen significant gains in early 2026, driven by the colder conditions and low storage. The low storage will support demand through the summer.

Renewable generation has generally been high this winter, with minimal periods of very low wind so far. The UK came close to blackouts in January 2025 as low winds tested the margins of spare capacity. This remains a risk going forward. Supply is now dependent on the global LNG market and therefore more prone than ever to geopolitical risk, plus weather conditions in the Far East and the US.

Having a contract in place reduces exposure to these risks, and Paul Davidson, our Business Development Manager at ConsultivUtilities, is ideally placed to offer advice and guidance on the ever-changing market conditions.